As 2022 comes to a close, it is an excellent time to review your finances and plan for the year ahead. Here are 5 financial boxes you should check off before the year ends.

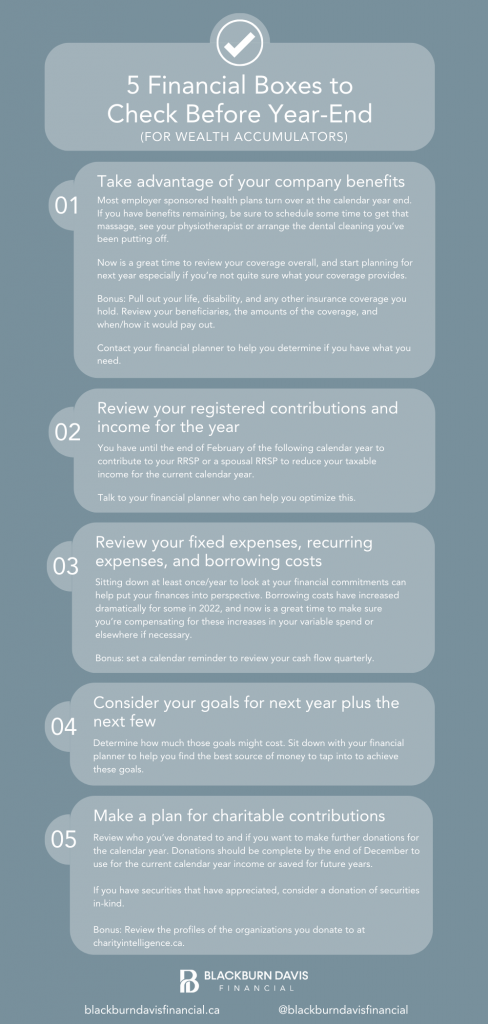

1 – Take advantage of your company benefits.

Most employer sponsored health plans turn over at the calendar year end. If you have benefits remaining, be sure to schedule some time to get that massage, see your physiotherapist or arrange the dental cleaning you’ve been putting off. Now is a great time to review your coverage overall, and start planning for next year especially if you’re not quite sure what your coverage provides. Bonus: Pull out your life, disability, and any other insurance coverage you hold. Review your beneficiaries, the amounts of the coverage, and when/how it would pay out. Contact your financial planner to help you determine if you have what you need.

2 – Review your registered contributions and your income for the year.

You have until the end of February of the following calendar year to contribute to your RRSP or a spousal RRSP to reduce your taxable income for the current calendar year. Talk to your financial planner who can help you optimize this.

3 – Review your fixed expenses, recurring expenses and your borrowing costs.

Sitting down at least once/year to look at your financial commitments can help put your finances into perspective. Borrowing costs have increased dramatically for some in 2022, and now is a great time to make sure you’re compensating for these increases in your variable spend or elsewhere if necessary. Bonus: set a calendar reminder to review your cash flow quarterly.

4 – Consider your goals for next year plus the next few.

Determine how much those goals might cost. Sit down with your financial planner to help you find the best source of money to tap into to achieve these goals.

5 – Make a plan for charitable contributions.

Review who you’ve donated to and if you want to make further donations for the calendar year. Donations should be complete by the end of December to use for the current calendar year income or saved for future years. If you have securities that have appreciated, consider a donation of securities in-kind. Bonus: Review the profiles of the organizations you donate to at charityintelligence.ca.

If you need assistance with any of these financial planning items before year-end, please reach out to us.

This is a common question that most start to consider as they approach their retirement years. There are typically 3 phases of retirement spending that one will age through. Watch this video to learn more.

Today we’re going to talk about how much you need to retire, which is a very common question that everyone eventually asks when they’re thinking about their future years. And the answer is really not simple. However, a good gauge is how much you’re currently spending.

Most retirees find that they don’t spend a whole lot less from their working years to their retirement years. Especially in the early stages of retirement. So a good planning strategy is to make sure that you’ve got enough of a retirement income when you’re starting retirement to approximate what you’re spending in your working years.

None of us know when our expiry date is, which is a factor in understanding how much you’ll need to save to provide you with that income for a lifetime. If we knew, it would be a lot easier to plan. But what you can do is make sure that you’re looking at where all of your assets are going to be coming from. Some people have pensions through work, and of course, all of the dollars that we save for our retirement will be added together to provide that income in retirement.

Having a proper financial plan completed along with projections to ensure you know where your income is going to be coming from in your retirement, how that’s going to be taxed, and what your net result will be is very important.

When you enter retirement, we find that there tends to be three phases of retirement income needs. In your early years of retirement, you’re going to need an income quite similar to your working years as this is typically when you are in your best health and interested in pursuing some of the hobbies and activities that you didn’t have time to pursue when you were working. That typically lasts from the time that you retire until maybe 75 or 80.

Once you hit your 80s, for most people they’re going to slow down and so will your spending. Oftentimes, the spending shifts from things that you might want to buy or do to being able to shift some of your wealth to the next generation. You might be thinking about giving money to children or grandkids. And you may be just done with travel and some of the major expenditures that people tend to pursue in their early retirement years. You will still spend money, and you want to make sure you have enough income to meet the needs of those years, but it will change.

The final phase of retirement spending is the later years of retirement. That third phase tends to be a lot of a slower spend, however, the challenge with the third phase of retirement is that sometimes there are healthcare costs. Healthcare costs can be really difficult to predict. We don’t know if somebody is going to need care, and it can be particularly challenging for couples. If one person needs care while the other is able to remain at home, you can end up having double the costs of living at this stage of life.

It is really important to build a buffer into your retirement plan so that if need be, you have assets available for that phase of life and potential healthcare costs that could arise.

If you haven’t done a projection, please reach out to your advisor so that you have a good understanding of what your retirement income is going to look like and that you have everything you need to make your retirement comfortable. You can learn more about our retirement planning services and approach here.

In this edition of Questions From Clients, Kelley Doerksen, CFP®, CIM® explains how RESPs (Registered Education Savings Plans) work. Learn about some of the key concepts surrounding RESPs such as grants, contributions, and withdrawals.

RESPs are a very effective way to save money for your child’s post-secondary education as you receive grants from the Government when you make contributions to the RESP.

An RESP will provide you with a 20% grant from the Government when you make contributions. You can receive up to $500 a year in grants. However, if you’ve missed some years of making contributions, you can go back and you can receive up to $1000 a year of the current year’s grants and previous year’s missed grants. You can continue to receive grants for your child until your child is 17, so long as you’ve started making contributions prior to their age 16.

When you go to withdraw from an RESP, although there are some rules and regulations, it’s actually fairly simple. When your student starts University or Post-Secondary, so long as they’re in a qualified post-secondary institution, you can begin withdrawals.

The student will need to provide proof of enrolment, and from there, RESP withdrawals can be made. There is no limit to how many dollars of contributions that can be taken out, however in the first year of school, there is a limit to the amount of grants and growth that can be withdrawn during the first 13 weeks of school.

The nice thing about an RESP is that your contributions have already been taxed when you’ve made the contribution initially to the RESP, and you won’t pay any tax on the contributions when they are withdrawn.

The grants and the growth are going to be taxed in the hands of your child. Many students don’t pay tax or pay very minimal tax while they’re students in University; therefore an RESP is a very effective way to income split from your assets to your child and potentially see no tax on the grants and the growth when that withdrawal is made.

To learn more about the terminology and specific rules pertaining to RESP accounts, please watch this video. If you have questions about how to use an RESP, please contact us and we’d be happy to help.

One of the objectives of estate planning is to review and minimize potential taxes on your remaining assets.

Lets review how some common assets (RRSP/RIFs, TFSAs, Non-Registered Accounts, and Principal Residences) are taxed upon death.

RRSP (Registered Retirement Savings Plan) / RIF (Retirement Income Fund)

The accounts can be left to a spouse as a named beneficiary. This transaction will generate a tax slip, but this is not a taxable event. The spouse can receive the proceeds of the RRSP/RIF.

In some circumstances, the RRSP/RIF could also pass to a dependent child without triggering tax.

TFSA (Tax-Free Savings Account)

No tax and no reporting is necessary.

If a spouse is named as the successor owner, the full value of the TFSA can become the spouse’s with no tax impact (even if the successor owner spouse may have no TFSA room available).

You can name beneficiaries such as children, and the assets would be provided once appropriate legal requirements are met after death.

Non-Registered Account

Death is a taxable disposition and all assets are deemed disposed on the date of death (meaning they are considered sold). The applicable gain or loss must be considered and tax paid.

Principal Residence

No tax is owing on the sale of a principal residence, however it must be noted when filing taxes that the property was deemed disposed.

If you have a question pertaining to your specific financial situation or need some assistance with estate planning, please reach out and our financial advisors would be happy to assist you. You can learn more about the estate planning services we provide here.

We invite you to join us for an upcoming webinar, Protecting Your Estate hosted by Daniel Collison on March 16, 2022 7:00-8:00pm. Register for the webinar here. The registration form enquires who invited you to this event – please fill ‘Blackburn Davis Financial’ in this field. Please feel free to pass this invitation along to any family member or friend you think would find it useful.

If you have any questions or would like further information about this event or speaker, please reach out to us.