This is Part 2 in our 3-part series on RDSP accounts or Registered Disability Savings Plans.

Today we are talking about working with RDSPs.

RDSPs are an effective way to save for your child’s financial future, or for your own if you are age of majority.

RDSPs can be started if you are eligible for the disability tax credit.

Contributions can be made to an RDSP up to a lifetime maximum of $200,000. Grants can also be earned in an RDSP – the government will contribute up to $70,000. Bonds can be paid into an RDSP from the government as well and bonds can be paid up to $20,000. Bonds are based on income – family income or your personal individual income; and it is a lower income threshold than grant contributions. You can consult the current legislation for the amount of income on an annual basis. Grants will be paid to an RDSP based on contributions and can be paid up to 300% of any contribution that has been made.

A contribution can attract up to $3,500 of grant money with a $1,500 contribution if family income is under, currently, about $100,000. And that can be collected back on years that grants may not have been applied for or one was eligible, but did not open an RDSP in time. You can go back up to 10 years to collect unearned but eligible grants in an RDSP.

RDSP withdrawals are designed such that an RDSP is kept open for the long-term financial security of the beneficiary of the RDSP. If withdrawals are made within 10 years of a grant or bond being paid into the account, there can be a proportionate claw back on withdrawals, and grants and bonds may need to be paid back to the government to some extent. Therefore, waiting for 10 years before withdrawals are made, is usually a really effective way to maintain the integrity of the account.

When withdrawals are made, you can withdraw in two formats. One is a Disability Assistance Payment or a DAP, and that’s a one-time lump sum withdrawal that might be made. An LDAP or a Lifetime Disability Assistance Payment is made or has to be started by the time the beneficiary is age 60. And it’s an annual recurring amount that needs to be withdrawn on a regular basis. There are some minimum and maximum requirements on an LDAP withdrawal, and it is dependent on a number of factors within the RDSP account.

You may be wondering what the difference is between a holder of an RDSP and the beneficiary. The holder of the RDSP is the individual who makes the decisions on the account. The beneficiary is the one who receives the benefit of the RDSP account. Many times the holder and the beneficiary are the same individual, but that is not always the case. For example, if the beneficiary is a minor, oftentimes the parents or guardian will be the holder of the RDSP account. And grants and bonds will be based on any income of the beneficiary’s family or parents in that circumstance. When the beneficiary and holder are the same individual, the beneficiary has to be at least 18 years of age and has to have capacity to make decisions on their own.

Parents can maintain the holder status on their child’s RDSP account, even if the child is 18 years of age or older, if the parent is the legal guardian of the child still.

RDSPs can be some of the most important dollars that families save for their loved ones, but they are also very complex. If you have any further questions, please reach out to us and we’re happy to discuss.

Today we’re talking about another common question from clients – what is a RIF and how does it work?

A RIF is simply a conversion from your Registered Retirement Savings Plan (RRSP) to a Registered Retirement Income Fund. So the income version of the tax sheltering that you receive from a registered account. A RIF is set up so you can continue to enjoy growth on your assets without paying tax as the assets grow.

Of course, you are going to be taxed when you take money out of your RIF. So how does that work?

You have to convert your RRSP to a RIF at age 71, and you must begin to draw income out of the RIF at age 72.

You can convert to a RIF prior to that if you choose to. You can also convert partially to a RIF from your RRSP account if you choose to, which can be a great way for you to use the pension tax credit for example.

So how much do you take out of a RIF when it’s time to convert? You have to take out a designated amount that’s specified by the Government as a percentage of your assets. Your assets will be calculated on December 31 of the previous calendar year and a percentage applied to it based on what CRA determines. This will give the minimum amount that you have to take out of your RIF once it’s in RIF format. You can always take more out of your RIF if you choose.

When you take money out of your RIF, it is taxed as ordinary income. The RIF minimum will not be taxed immediately, but you need to consider it in your tax planning for the year. Anything over and above RIF minimum will incur a withholding tax, and that portion will be taxed as you go. You can ask to have your RIF minimum taxed as you go as well, but it’s not automatic.

Another common question we get asked is whether you are taxed twice on a RIF? And the answer to that is absolutely not.

When you make a contribution to your RRSP in your working years, typically you are at a much higher income than you are in your retirement years. Often this means you get a great tax benefit throughout your working career to make those RRSP contributions. Following that up, you pay a much lower rate of tax when you draw that money out from your RIF.

So are you taxed on your RIF? Absolutely, but you’re certainly not double-taxed. And typically, you are seeing a significant benefit in terms of tax planning from your working career to your retirement years.

If you have any questions about how your RIF fits into your financial plan, please contact your advisor or give us a call.

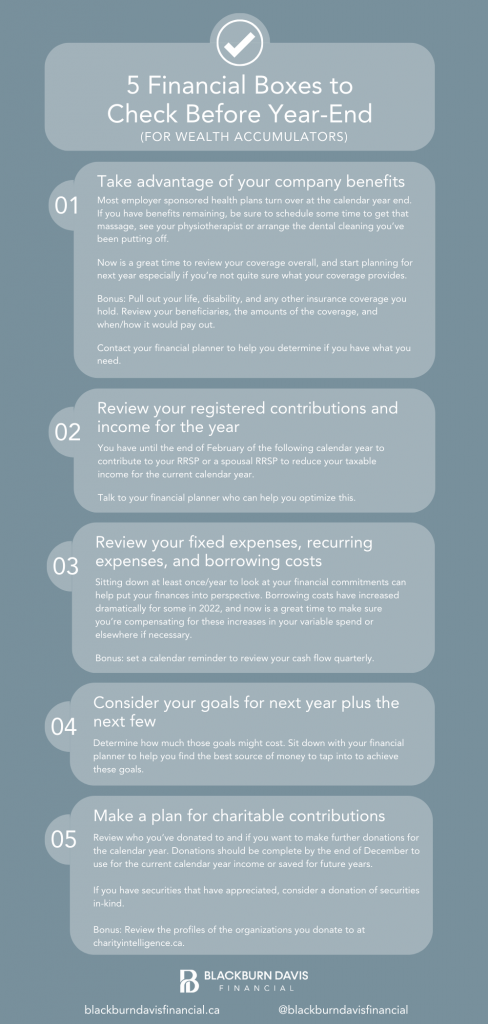

As 2022 comes to a close, it is an excellent time to review your finances and plan for the year ahead. Here are 5 financial boxes you should check off before the year ends.

1 – Take advantage of your company benefits.

Most employer sponsored health plans turn over at the calendar year end. If you have benefits remaining, be sure to schedule some time to get that massage, see your physiotherapist or arrange the dental cleaning you’ve been putting off. Now is a great time to review your coverage overall, and start planning for next year especially if you’re not quite sure what your coverage provides. Bonus: Pull out your life, disability, and any other insurance coverage you hold. Review your beneficiaries, the amounts of the coverage, and when/how it would pay out. Contact your financial planner to help you determine if you have what you need.

2 – Review your registered contributions and your income for the year.

You have until the end of February of the following calendar year to contribute to your RRSP or a spousal RRSP to reduce your taxable income for the current calendar year. Talk to your financial planner who can help you optimize this.

3 – Review your fixed expenses, recurring expenses and your borrowing costs.

Sitting down at least once/year to look at your financial commitments can help put your finances into perspective. Borrowing costs have increased dramatically for some in 2022, and now is a great time to make sure you’re compensating for these increases in your variable spend or elsewhere if necessary. Bonus: set a calendar reminder to review your cash flow quarterly.

4 – Consider your goals for next year plus the next few.

Determine how much those goals might cost. Sit down with your financial planner to help you find the best source of money to tap into to achieve these goals.

5 – Make a plan for charitable contributions.

Review who you’ve donated to and if you want to make further donations for the calendar year. Donations should be complete by the end of December to use for the current calendar year income or saved for future years. If you have securities that have appreciated, consider a donation of securities in-kind. Bonus: Review the profiles of the organizations you donate to at charityintelligence.ca.

If you need assistance with any of these financial planning items before year-end, please reach out to us.

As we approach the end of the year, some clients may have questions about capital gains and losses that have occurred in their portfolio.

Watch this video to understand what capital gains and losses are and how they may impact your taxes.

Today we are discussing capital gains and losses.

Capital gains and losses are in reference to a taxable account and today we are discussing them as they relate to stocks, although capital property is another variety of property that they can apply to.

Capital gains and losses occur when you dispose of a stock at higher or lower than your adjusted cost base (ACB).

Your adjusted cost base (ACB) is the total price that you have paid for your stock. In addition, you can add some of the cost that you had to acquire the stock, such as commissions, to the adjusted cost base.

A capital gain occurs when you sell your stock for more than your adjusted cost base. A capital loss occurs when you sell your stock for less than the adjusted cost base.

Capital Gain

Let’s say you paid $100 for your stock and you sell it for $150. You would have a capital gain of $50 – the difference between your sale price, and in this example, your adjusted cost base.

Halfof the $50 is taxable, so $25 would be taxable for you in the year that you dispose of the security.

Capital Loss

Conversely a capital loss would happen if you sold your security for $75.

You’ve incurred a loss of $25 and halfof that – $12.50,can be used to reduce any capital gains that you’ve experienced in the year that you’ve sold your security, three years prior, or essentially indefinitely going forward.

Capital gains and losses are in reference to a taxable account (Non-Registered Accounts). They do not apply to Registered Retirement Savings Plans (RRSPs) or Tax-Free Savings Accounts (TFSAs).

Capital gains and losses can be used for tax planning, so please reach out to our team if you have a tax planning situation that you need assistance with. Learn more about the tax planning services we provide here. If you have any further questions about capital gains and losses, contact us here.

One of the objectives of estate planning is to review and minimize potential taxes on your remaining assets.

Lets review how some common assets (RRSP/RIFs, TFSAs, Non-Registered Accounts, and Principal Residences) are taxed upon death.

RRSP (Registered Retirement Savings Plan) / RIF (Retirement Income Fund)

The accounts can be left to a spouse as a named beneficiary. This transaction will generate a tax slip, but this is not a taxable event. The spouse can receive the proceeds of the RRSP/RIF.

In some circumstances, the RRSP/RIF could also pass to a dependent child without triggering tax.

TFSA (Tax-Free Savings Account)

No tax and no reporting is necessary.

If a spouse is named as the successor owner, the full value of the TFSA can become the spouse’s with no tax impact (even if the successor owner spouse may have no TFSA room available).

You can name beneficiaries such as children, and the assets would be provided once appropriate legal requirements are met after death.

Non-Registered Account

Death is a taxable disposition and all assets are deemed disposed on the date of death (meaning they are considered sold). The applicable gain or loss must be considered and tax paid.

Principal Residence

No tax is owing on the sale of a principal residence, however it must be noted when filing taxes that the property was deemed disposed.

If you have a question pertaining to your specific financial situation or need some assistance with estate planning, please reach out and our financial advisors would be happy to assist you. You can learn more about the estate planning services we provide here.